Sovereign AI vs. Tariff Turbulence: Nvidia, AMD & CoreWeave’s Next Frontier

Welcome, AI & Semiconductor Investors,

When governments double down on national “AI factories” even as Washington tightens export screws, the semiconductor battleground shifts in real time. Today, we dissect Citi’s $190 Nvidia rebound amid tariff jitters, chart AMD’s pivot from standalone GPUs to Helios-powered systems, and drill into CoreWeave’s $9 billion power-capacity merger.— Let’s Chip In

What The Chip Happened?

📰 Nvidia’s Sovereign AI Sizzle vs. Tariff Fizzle

🔧 AMD’s Racks, Ramps & Re‑Ratings

⚡ Power Up: CoreWeave locks in 1.3 GW by buying Core Scientific for “$9B”

[Penguin Solutions in plain English]

Read time: 7 minutes

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Nvidia (NASDAQ: NVDA)

📰 Sovereign AI Sizzle vs. Tariff Fizzle

What The Chip: On July 7 2025, Citi’s Atif Malik hiked Nvidia’s price target to $190 on surging government‑funded AI demand—even as the stock dipped on fresh U.S.–China tariff fears.

The Situation Explained:

🚀 Macro TAM upgrade. Citi now pegs the 2028 AI–data‑center TAM at $563 bn (+13 %) and networking TAM at $119 bn (+32 %), calling sovereign “AI factories” a brand‑new spending wave.

💰 Margin stamina. Malik models Blackwell GB200/GB300 ramps plus richer networking attach keeping gross margins in the mid‑70 % range through FY‑26.

📈 Mizuho backs the bull case. Analyst Vijay Rakesh lifted his PT to $185 and argues Blackwell “sets the de‑facto standard” through 2027, pushing FY‑26 revenue to $202 bn and valuing NVDA at 32.7× FY‑27 EPS.

🌏 Plan B for China. Rakesh highlighted a planned “B40” accelerator for China—latent upside if export rules relax.

⚠️ Tariff overhang. Traders fixated on possible new U.S. curbs that CEO Jensen Huang warned could slice ~$15 bn from revenue, turning Citi’s dip into what it called “a gift.”

🏛️ Sovereign cloud decoupling. Citi contends national AI clusters will keep capex growing even if commercial budgets cool, underpinning its 30 × FY‑28 P/E assumption.

Why AI/Semiconductor Investors Should Care: Sovereign AI spending gives Nvidia a multi‑year runway that could offset export‑control speed bumps and justify premium multiples. Yet headline risk around China remains the swing factor for sentiment—and potential entry points. Keep an eye on Blackwell’s rollout pace and Washington’s tariff cadence; together they decide whether Citi’s $190 thesis sticks.

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Advanced Micro Devices (NASDAQ: AMD)

🔧 Racks, Ramps & Re‑Ratings

What The Chip: Between June 16 – July 7 2025, four brokers lifted AMD targets—yet opinions split on whether the Instinct and Helios road map warrants a true multiple break‑out.

The Situation Explained:

🧐 Citi cautious but higher. Christopher Danely raised his PT to $145 (from $120) but kept a Neutral, calling the pull‑back “valuation‑driven” until MI300 volumes and software depth improve.

🔄 Mizuho math shift. Vijay Rakesh bumped the PT to $152, applying a 25.9× FY‑26 EPS multiple after modeling a slightly better MI355X ramp in 2H‑25; heavy R&D trims FY‑25 EPS to $3.90.

🚀 Melius upgrade. Ben Reitzes flipped to Buy and shot the target to $175, forecasting EPS > $8 by 2027 as AI inferencing demand broadens and Nvidia wait‑times frustrate hyperscalers.

🖥️ Systems‑level story. Piper Sandler’s PT jump to $140 cites the Helios rack (up to 72 MI400 GPUs, shipping in 2026) and new deals with OpenAI, Meta, Oracle, and Microsoft—plus chatter that AWS may join.

⚠️ Software gap is still real. Citi argues that ROCm and ecosystem depth must catch up to CUDA before Wall Street awards a sustained premium multiple.

💸 R&D squeeze. Bigger accelerator road maps mean near‑term earnings dilution—one reason Citi remains on the sidelines despite a headline 21 % upside to fair value.

Why AI/Semiconductor Investors Should Care: The street’s enthusiasm is migrating from standalone GPUs to systems—Helios‑style racks that bundle silicon, software, and service contracts. If AMD executes on MI355X/MI400 ramps and tightens its software stack, upside targets (> $150) look credible. Miss those milestones, and Citi’s valuation‑driven skepticism wins out. For investors, the bet is on execution speed and ecosystem stickiness—both now priced into expanding (but fragile) multiples.

CoreWeave (NASDAQ: CRWV)

⚡ Power Up: CoreWeave locks in 1.3 GW by buying Core Scientific for “$9B”

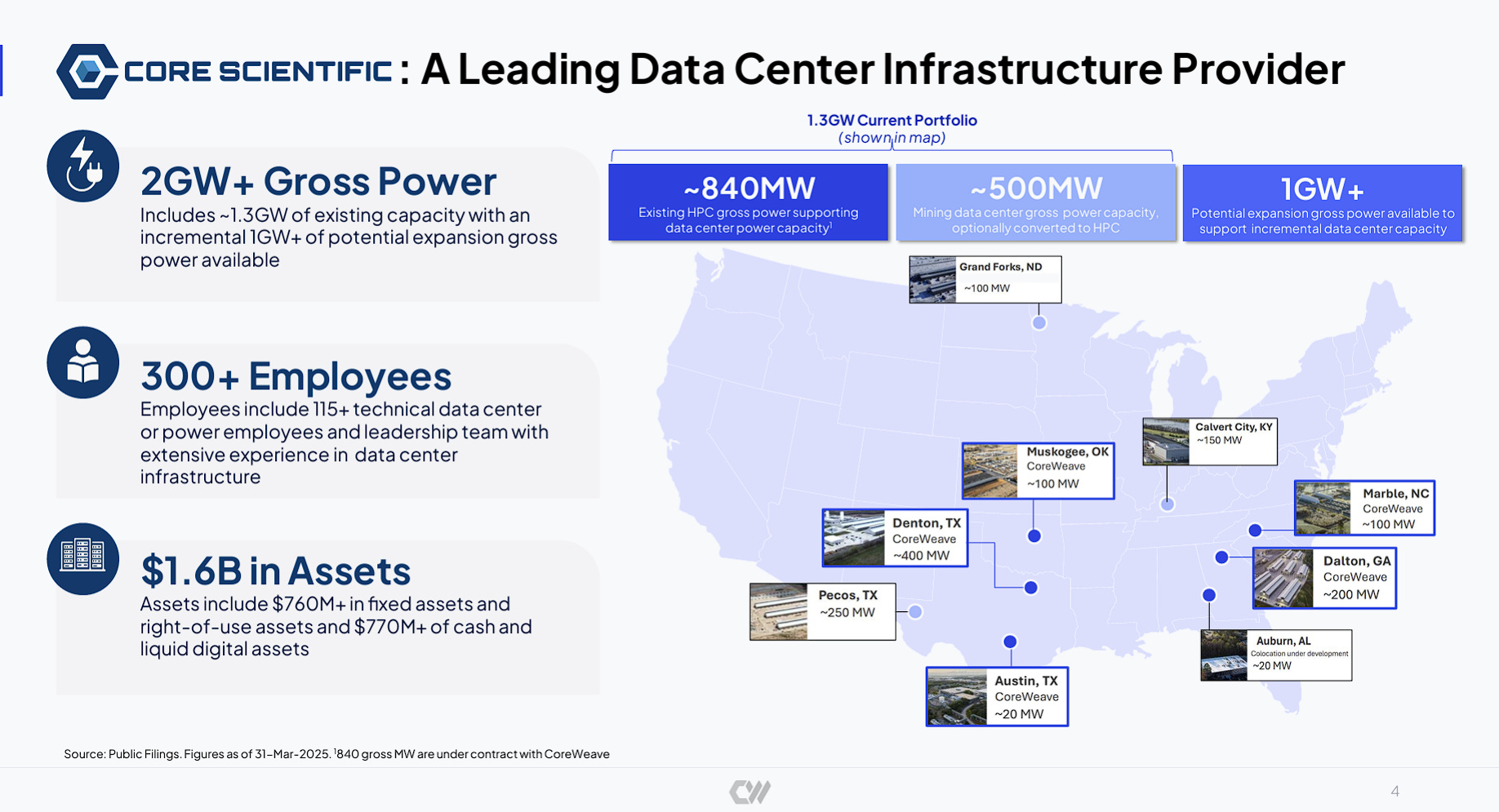

What The Chip: In an all‑stock deal announced on July 7, 2025, CoreWeave agreed to acquire bitcoin‑miner‑turned‑AI‑infrastructure‑operator Core Scientific (NASDAQ: CORZ) for roughly $9 billion in equity, issuing 0.1235 CRWV shares for every CORZ share. Management says the merger “verticalizes” >1.3 GW of power capacity and should close in Q4 2025.

The Situation Explained:

🔄 100 % stock‑for‑stock. Core Scientific holders will own < 10 % of the combined company after closing.

💲 Exchange ratio = 0.1235. At CRWV’s pre‑deal VWAP, that implies $19.7 per CORZ share—yet CORZ trades near $14.83, a 25 % discount that signals deal‑risk and CRWV‑hedging pressure.

⚡ 1.3 GW secured. Core Scientific brings ~840 MW contracted plus >500 MW expansion potential, cutting CoreWeave’s reliance on costly leases.

✂️ Cost wins. Eliminating leases removes >$10 B of future payments and targets $500 M annual run‑rate savings by 2027.

🏗️ Dilution contained. Issuing ~37 M new shares (≈15 % of CRWV’s base) buys $9 B of assets—far less dilutive than funding the same purchase at the $40 March IPO price.

📉 Initial market read. On headline day CRWV fell ~3 % while CORZ plunged ~18 %, reflecting arbitrage activity and execution risk.

🗣️ CEO sound bites. “This acquisition accelerates our strategy to deploy AI and HPC workloads at scale,” said CoreWeave CEO Michael Intrator. Core Scientific CEO Adam Sullivan called the tie‑up “the greatest value for our shareholders.”

Why AI/ Semiconductor Investors Should Care: Vertical ownership of cheap, scalable power is emerging as the tightest bottleneck in the AI compute arms race. By swapping pricey leases for owned megawatts, CoreWeave can lower its cost of capital and safeguard margins—even if GPU prices or AI demand wobble. The flip side: investors must weigh integration risk, added capital intensity for liquid‑cooling retrofits, and the >25 % spread that hints at lingering skepticism around AI‑infrastructure valuations. In short, the deal could super‑charge CoreWeave’s moat—provided management executes before the AI cycle cools.

Youtube Channel - Jose Najarro Stocks

X Account - @_Josenajarro

Get 15% OFF FISCAL.AI — ALL CHARTS ARE FROM FISCAL.AI —

Disclaimer: This article is intended for educational and informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.

The overview above provides key insights every investor should know, but subscribing to the premium tier unlocks deeper analysis to support your Semiconductor, AI, and Software journey. Behind the paywall, you’ll gain access to in-depth breakdowns of earnings reports, keynotes, and investor conferences across semiconductor, AI, and software companies. With multiple deep dives published weekly, it’s the ultimate resource for staying ahead in the market. Support the newsletter and elevate your investing expertise—subscribe today!

[Paid Subscribers] Penguin Solutions in plain English

Date of Event: Various events, just consolidated data.

Executive Summary

*Reminder: We do not talk about valuations, just an analysis of the earnings/conferences

Penguin Solutions, Inc. designs, builds, and supports the “plumbing” that lets organisations run demanding artificial‑intelligence (AI) and other high‑performance workloads at scale. The company sells three distinct but complementary lines of business that map onto the hardware, software, and services most data‑centre operators need:

Penguin drops FQ3‑25 results today (July 8, 2025, 4:30 p.m. ET) after front‑loading Blackwell GPU‑cluster shipments in H1. Wall Street looks for revenue $330.8 M (+10 % YoY) and non‑GAAP EPS $0.33, but options price a ±10–11 % swing.

1. Advanced Computing

Revenue Q2 FY25: USD 200 million (55 % of total)

What it is. Turn‑key clusters that combine graphics processing units (GPUs), CPUs, networking, memory, storage, power and cooling—plus the software to manage it all.

Flagship software. ICE ClusterWare™ delivers cluster management, workload scheduling, health monitoring, and, since March 2025, multi‑tenant support and an AIM optimisation service that predicts failures and improves uptime.

Services layer. Penguin’s engineers design the rack‑level architecture, install it on‑site, and often run it day‑to‑day under multi‑year managed‑services contracts.

Who buys.